General Administration of Financial Supervision: The financial industry is duty-bound to strongly support real estate.

"The General Administration of Financial Supervision will comprehensively strengthen financial supervision, prevent and resolve financial risks, fully hold the bottom line of no systemic risks, and do a good job in the’ five big articles’ on technology and finance, green finance, inclusive finance, pension finance and digital finance, so as to provide strong financial support for high-quality economic and social development and the realization of Chinese modernization and the great rejuvenation of the Chinese nation." On January 25, Xiao Yuanqi, deputy director of the General Administration of Financial Supervision, said at the press conference on the theme of "High-quality economic and social development of financial services" of the State Council Office.

Also present at the above conference were Li Mingxiao, spokesperson of the General Administration of Financial Supervision and Director of Policy Research Department; Liu Zhiqing, spokesperson of the General Administration of Financial Supervision and Director of Statistics and Risk Monitoring Department; Guo Wuping, Director of inclusive finance Department of the General Administration of Financial Supervision and Yin Jiangao, Director of Property Insurance Supervision Department of the General Administration of Financial Supervision.

Liu Zhiqing said that in recent years, the credit structure of the banking industry in China has been continuously optimized, and financial support for the real economy has become more precise and powerful. Financial resources have been more used in key areas and weak links of the national economy such as scientific and technological innovation, advanced manufacturing, green development, universal benefits, infrastructure, etc. We will continue to guide and support banking institutions to increase credit supply, optimize credit structure, focus on "five major articles", focus on unblocking the channels for funds to enter the real economy, and improve the efficiency of capital use, so as to "live water" with finance.

Last year, the net profit of commercial banks increased by 3.24%.

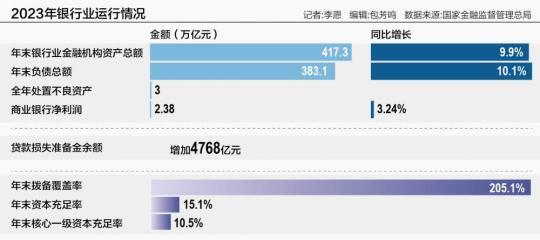

Regarding the operation of the banking and insurance industry in 2023, Liu Zhiqing said that the total assets and major businesses of the banking and insurance industry grew steadily. By the end of 2023, the total assets of banking financial institutions were 417.3 trillion yuan, a year-on-year increase of 9.9%, and RMB loans increased by 22.75 trillion yuan, an increase of 1.31 trillion yuan. Total liabilities amounted to 383.1 trillion yuan, up 10.1% year-on-year, and RMB deposits increased by 25.74 trillion yuan, down 510.1 billion yuan year-on-year.

According to preliminary statistics, the net profit of commercial banks in 2023 was 2.38 trillion yuan, a year-on-year increase of 3.24%. In contrast, in the first three quarters of 2023, commercial banks achieved a net profit of 1.9 trillion yuan, a year-on-year increase of 1.6%.

The quality of banking assets remained stable. According to preliminary statistics, by the end of 2023, the balance of non-performing loans of banking financial institutions was 3.95 trillion yuan, an increase of 149.5 billion yuan from the beginning of the year. The NPL ratio was 1.62% (1.65% at the end of the third quarter of 2023). The ratio of loans overdue for more than 90 days to non-performing loans in commercial banks is 84.2%, which remains at a low level. 3 trillion yuan of non-performing assets were disposed of in the whole year (since 2017, the cumulative disposal of non-performing assets of banks reached 18 trillion yuan), and the disposal efforts were maintained.

The banking industry has sufficient risk compensation capacity. By the end of 2023, the balance of loan loss reserves of commercial banks had increased by 476.8 billion yuan, and the provision coverage ratio was 205.1%, which remained at a high level. The capital adequacy ratio is 15.1%, and the core tier 1 capital adequacy ratio is 10.5%. Among them, the capital adequacy ratio of large banks is 17.6%, and the core tier 1 capital adequacy ratio is 11.7%.

"In 2024, the banking industry is expected to maintain a steady development momentum, with more reasonable institutional and functional layout and further optimization of financial resource allocation. In the past three years, the average growth rate of total assets of the insurance industry reached 8.7%, maintaining a good development trend. The insurance industry has great potential for future development, and its ability to serve the overall social and economic situation will continue to increase, and the functions of economic shock absorbers and social stabilizers will be more effectively exerted. " Liu Zhiqing said.

A series of real estate policies have shown results.

At the press conference, the General Administration of Financial Supervision also introduced the real estate market and small and medium-sized financial institutions that are highly concerned by the market.

Xiao Yuanqi said that the real estate industry has a long chain and a wide range, which has an important impact on the national economy and is closely related to the lives of the broad masses of the people. The financial industry is duty-bound and must be strongly supported. It is also disclosed that in 2023, banking institutions issued 3 trillion yuan of development loans and 6.4 trillion yuan of housing mortgage loans respectively, which add up to nearly 10 trillion yuan. Up to now, the balances of development loans and personal housing loans are 12.3 trillion yuan and 38.3 trillion yuan respectively; By the end of 2023, the balance of bonds purchased by banks from real estate enterprises was 427.5 billion yuan; Providing M&A loans and stock extension loans to real estate enterprises add up to more than 1 trillion yuan.

Xiao Yuanqi said that recently, the General Administration of Financial Supervision, together with relevant departments, has issued a series of measures to support the real estate market. "These policies and measures have played and are playing an active role in doing a good job in real estate financial services, stabilizing the reasonable financing demand of the real estate market and promoting the stable and healthy development of real estate."

"In the near future, we will also focus on the following major tasks: First, we will accelerate the implementation of the coordination mechanism for urban real estate financing, and will hold relevant work deployment meetings, requiring banks to act as soon as possible and make good use of the policy toolbox because of the city’s policy; The second is to guide financial institutions to implement the management requirements of operating property loans; Third, continue to do a good job in personal housing loan financial services, support local city governments and housing construction departments, and further optimize personal housing loan policies such as down payment ratio and loan interest rate due to city policies; The fourth is to guide and require banks and other financial institutions to vigorously support the construction of’ three major projects’ such as the transformation of urban villages, and to form physical workload as soon as possible. " Xiao Yuanqi said.

Regarding the risk situation of small and medium-sized financial institutions, Xiao Yuanqi said that from a nationwide perspective, the current small and medium-sized banks are operating steadily, their asset quality is stable, and their capital strength is significantly enhanced. The capital adequacy ratio, provision coverage ratio and asset quality of small and medium-sized banks are generally at a relatively good level, and these operating and regulatory indicators are at a reasonable and healthy level.

Xiao Yuanqi said that the General Administration of Financial Supervision will work closely with local party committees, governments and relevant departments to do a good job in the reform and risk prevention and control of small and medium-sized banks, and constantly improve their management level: first, strengthen corporate governance; second, select top executives and key personnel; third, deepen reform through classified policies; fourth, urge small and medium-sized banks to focus on their main business; fifth, adhere to goal-oriented and problem-oriented, strive for progress while addressing both the symptoms and root causes, and comprehensively strengthen supervision and prevention.

Do a good job of "five big articles"

The Central Financial Work Conference pointed out that high-quality development is the primary task of building a socialist modern country in an all-round way, and finance should provide high-quality services for economic and social development, and it is required to do "five major articles" well. At the press conference, the General Administration of Financial Supervision made a detailed introduction on the "five big articles" and the next step plan.

In technology and finance, Li Mingxiao disclosed that by the end of 2023, the loan balance of high-tech enterprises nationwide had increased by 20.2% year-on-year, of which medium and long-term loans and credit loans accounted for more than 40%. By the end of 2023, the loan balance of manufacturing industry increased by 17.1% year-on-year, of which the medium and long-term loan balance of manufacturing industry increased by 29.1% year-on-year.

"Promote the improvement of the multi-level service system in technology and finance. Under the premise of risk control, we will steadily promote the construction of the pilot zone for science and technology innovation and financial reform with relevant departments, deepen the financial support measures for manufacturing, guide financial institutions to implement various policy requirements, and continuously enrich financial products and services. Continue to increase support for scientific and technological innovation and advanced manufacturing, help the development of new quality productive forces, and strive to provide strong financial support for accelerating the construction of a modern industrial system." For the next work plan, Li Mingxiao said.

In terms of green finance, Li Mingxiao disclosed that by the end of 2023, the green credit balance of 21 major banks had reached 27.2 trillion yuan, a year-on-year increase of 31.7%. In inclusive finance, Guo Wuping said that by the end of 2023, the balance of inclusive finance loans in the banking industry was 29.06 trillion yuan, a year-on-year increase of 23.27%, which was 13.13 percentage points higher than the average growth rate of various loans; The average interest rate of new loans for inclusive small and micro enterprises was 4.78%, down 0.47 percentage points year-on-year. "This year, we will implement the requirements of inclusive finance’s big article, integrate loans from small and micro enterprises, agriculture-related entities and private enterprises, form a unified regulatory caliber for inclusive credit, and carry out assessment and data disclosure." Guo Wuping said.

In terms of pension finance, Yin Jiangyao said that the General Administration of Financial Supervision will promote insurance institutions to give full play to the advantages of insurance protection and vigorously develop commercial insurance annuities. In terms of digital finance, Liu Zhiqing said that the General Administration of Financial Supervision will continue to promote the digital transformation of the banking and insurance industry, enhance the effectiveness of digital empowerment, enhance the industry’s risk prevention and control capabilities, strengthen network security and data security risk supervision, and standardize digital innovation.

(Author: Li Yuan)